The report examines India’s electricity transition under current policy scenarios (CPS) aligned with India’s Net Zero Scenario (NZS) by 2070 commitment.

- The power sector accounted for 39.4% of the country’s total GHG emissions in 2020 (MoEFCC, 2024).

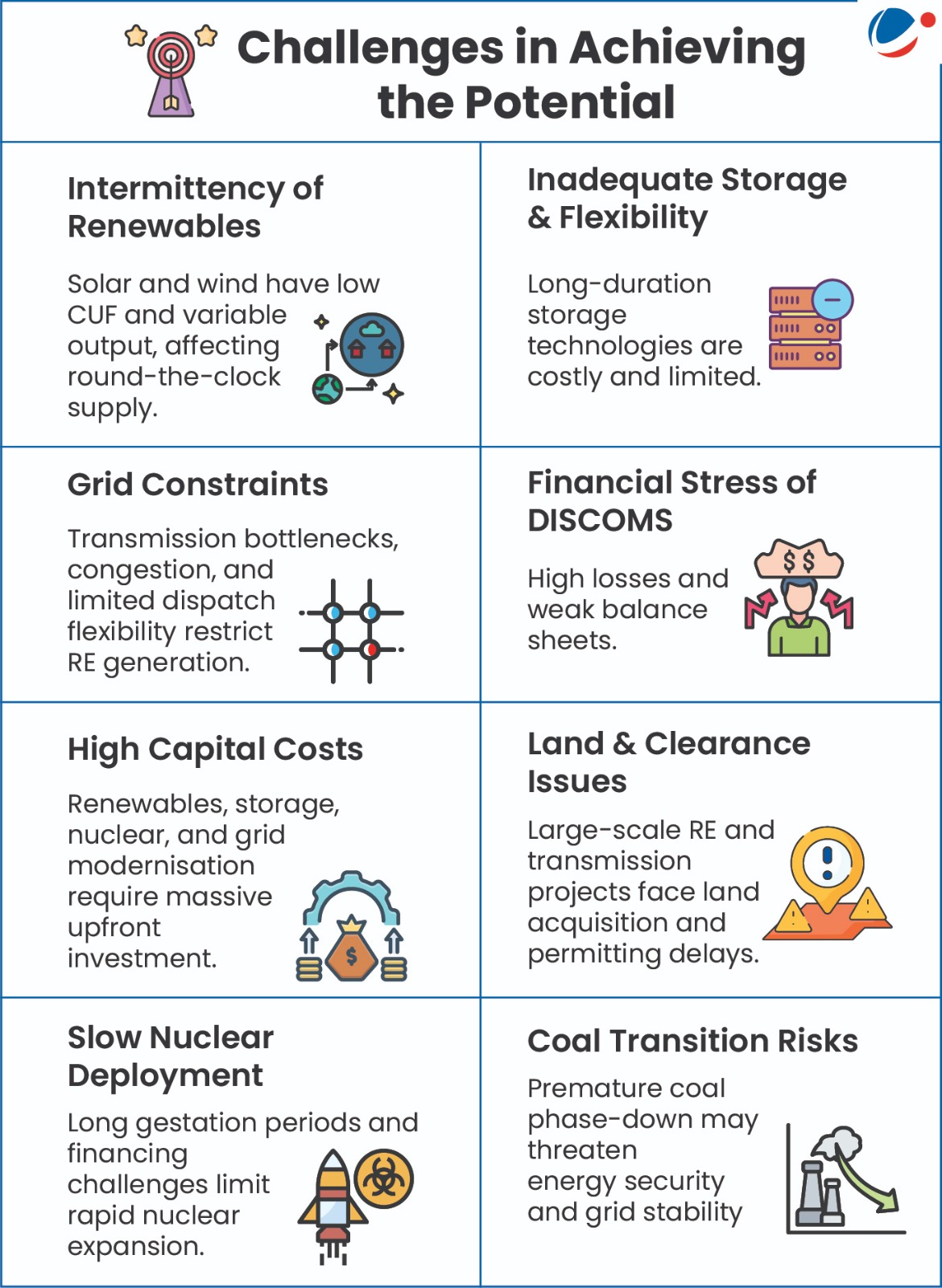

Key Projections

- Electrification-Led Demand: Electricity becomes the dominant energy carrier, with its share rising to 40% (CPS) and 60% (NZS) by 2070.

- Renewable Capacity Expansion: Installed capacity multiplies 9–14 times by 2070, with renewables supplying 90–93% of capacity, led by solar PV and wind, supported by distributed generation.

- Storage & Flexibility: A renewables-heavy grid requires massive storage deployment—up to 3,000 GW of batteries and 160 GW of pumped hydro power to ensure system stability.

- Nuclear as Firm Power: Nuclear capacity expands from 8.8 GW to over 300 GW by 2070, providing firm, low-carbon baseload power, with Small Modular Reactors (SMRs) enhancing flexibility.

Key Recommendations for India’s Power Sector

- Generation Sector: Scale solar–wind–storage hybrids, expand nuclear (SMRs), enable flexible coal operations, repurpose old plants, and incentivise energy storage.

- Transmission & Distribution: Expand Green Energy Corridors, digitise grids, reform DISCOMs, and promote competition through peer to peer trading.

- Policy & Regulatory Reforms: Deepen power markets, implement cost-reflective tariffs, strengthen renewable mandates, and institutionalise resource adequacy planning.

- Sustainability & Innovation: Strengthen domestic manufacturing via PLI, enforce recycling and cybersecurity norms, and use AI/ML for forecasting.

- Project Financing: Mobilise climate finance and green bonds and adopt GDF/PPP models to improve efficiency and investment flow.