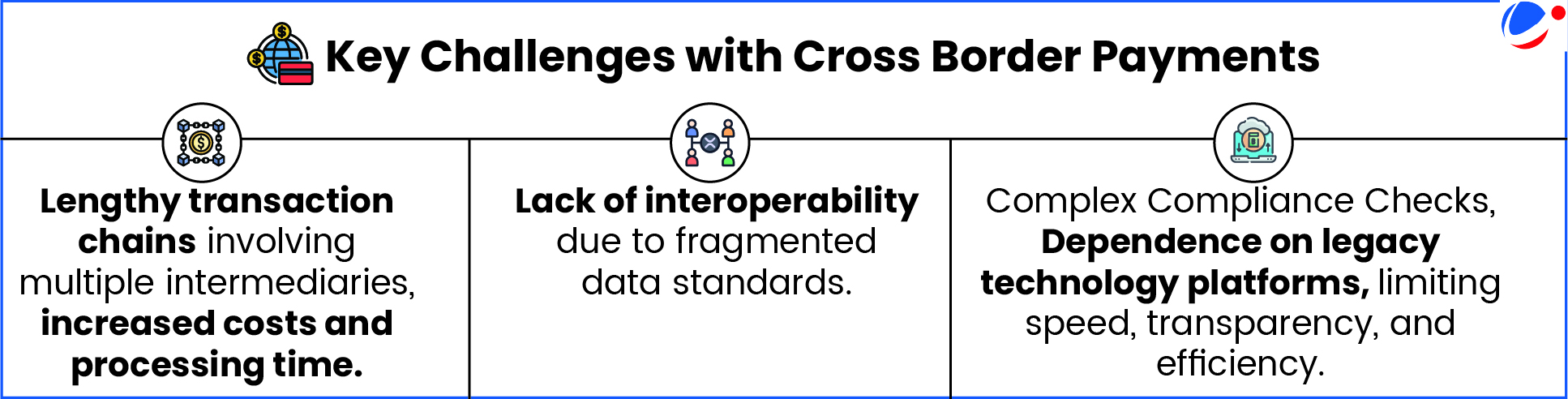

In its bi-annual Payment Systems Report, RBI cautions that sanctions, currency restrictions, and other operational barriers could disrupt seamless international transactions.

About Cross Border Payments

- Definition: These are financial transactions where the payer and the recipient are based in separate countries.

- They cover both wholesale and retail payments, including remittances.

- Two Main Types:

- Wholesale cross-border payments: Typically between financial institutions.

- Retail cross-border payments: Typically between individuals and businesses. E.g. person-to-person, person-to-business etc.

- Significance: Increased International mobility of goods and services, capital and people has contributed to its growing economic importance.

- Status in India: India remains the top recipient of global foreign remittances, with a record $137.7 billion inflow in 2024.

Initiatives to facilitate Effective Cross Border Payments

- Global

- G20 Roadmap: Addressing challenges like high cost, slow speed, limited access, and insufficient transparency, etc.

- Bank for International Settlements (BIS) Innovation Hub Projects: Like Project Hertha, Project Rialto, Project Agora etc.

- Others: Recommendations of Financial Stability Board (FSB) and the Committee on Payments and Market Infrastructure (CPMI), etc.

- India

- Bilateral/Multilateral collaboration: Linking UPI with foreign Fast Payment Systems (FPSs) of other countries via QR code acceptance of UPI at merchant locations abroad.

- E.g. UPI and PayNow (Singapore) Linkage, Project Nexus (a multilateral international initiative), etc.

- Bilateral/Multilateral collaboration: Linking UPI with foreign Fast Payment Systems (FPSs) of other countries via QR code acceptance of UPI at merchant locations abroad.