Why in the News?

Recently, US President issued an executive order for banning the establishment of USA's Central Bank Digital Currency (CBDC), i.e., 'Digital Dollar'.

What is Digital Currency?

- It is money that is exclusively available only in digital or electronic form.

- They are generally handled, preserved and exchanged using digital computer systems, connected to the Internet.

3 Types of Digital Currencies | ||

Cryptocurrency | CBDCs | Stablecoins |

|

|

|

About CBDC

- It is a legal tender and a central bank liability in digital form denominated in sovereign currency and appearing on central bank balance sheet. (RBI)

- Types of CBDCs

- Wholesale CBDCs: Used among banks and other licensed financial institutions for interbank payments and securities transactions.

- Retail CBDC: It is available to general public via digital wallets, smartphone apps, etc. Two models of retail CBDC:

- Token-based CBDCs: Enables anonymous transactions through private and public key authentication.

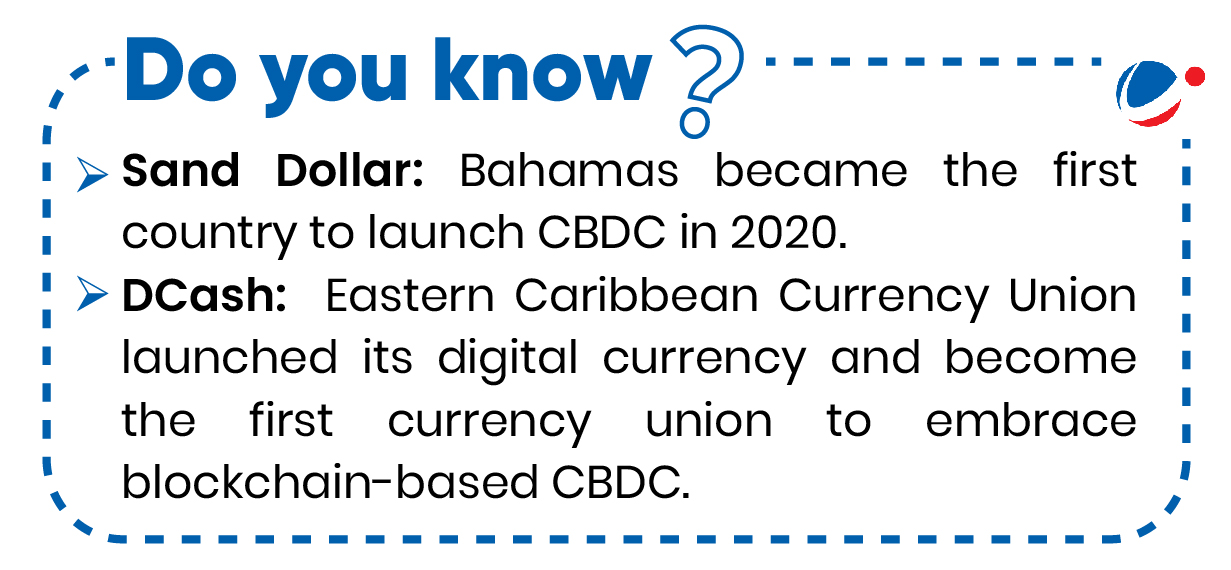

- Account-based CBDCs: Requires user digital identification for account access. e.g., DCash of Eastern Caribbean.

Potential benefits of CBDCs

About India's Digital Rupee (e₹)

|

- Financial inclusion: CBDCs can give unbanked or under-banked people access to digital payment services, allowing them to engage more fully in the economy.

- Reduced transaction costs: Elimination of intermediaries like commercial banks and payment processors reduces transaction fees for businesses and individuals.

- Reduced dependence on cash: Help in reducing the cost of printing, distributing, and managing physical currency.

- CBDCs operate on digital ledgers, allowing for better tracking of transactions, reducing corruption, tax evasion, and illicit activities.

- Improve monetary policy transmission: Central banks can implement direct stimulus measures, such as distributing funds instantly to citizens during economic crises, improving the effectiveness of monetary policy.

- Cross-Border Payment Efficiency: CBDCs can simplify and speed up international trade payments, reducing reliance on intermediaries like SWIFT.

- Programmable Payment Mechanisms: Digital currency transfers can be conditionally programmed, such as setting expiration dates or restricting spending to specific vendors.

Challenges with CBDCs

- Cybersecurity risks: CBDCs are vulnerable to cyberattacks, hacking, and data breaches, which could potentially compromise financial stability.

- Privacy Concerns: Transaction tracking and identity verification raise data protection issues.

- Digital divide: The complex technical requirements and need for digital literacy in using CBDCs could widen the gap between tech-savvy and less technologically adapted populations.

- International Regulatory Challenges: Cross-border use of CBDCs requires coordination between countries to prevent financial crimes, money laundering, and regulatory arbitrage.

- Technical variables such as different blockchain / Distributed Ledger Technology (DLT) standards and applications may reduce the efficiency of CBDCs across borders.

- Threat to Monetary Sovereignty: If people prefer a foreign CBDC (e.g., Digital Dollar or Digital Yuan) over their national currency, it could weaken the local monetary system.

Way Forward

- Balancing Privacy and Transparency: Use of technologies such as Zero-Knowledge Proofs (ZKPs) and privacy-preserving digital ledger solutions can ensure user privacy while enabling regulatory oversight.

- Zero-knowledge Proofs are a cryptographic method used to prove knowledge about a piece of data, without revealing the data itself.

- Monetary Policy and Fiscal Policy integration: Specific use-cases of CBDCs for Direct Benefit Transfers (DBTs), subsidies, and social security payments, etc., can be explored to improve economic efficiency.

- Regulatory and Legal Frameworks: States need to unambiguously define CBDC's and other digital currencies' legal status, liabilities, and consumer rights to prevent misuse.

- In this regard, regulatory sandboxes can be developed to test and refine CBDC policies before national rollout.

- Cross-border collaboration and standardization: Global community can work with international financial institutions (IMF, BIS, etc.) to establish global standards for CBDC interoperability and regulation.