Why in the News?

Defence Minister reiterated the Government's commitment to achieve Aatmanirbharta in defence manufacturing and make the country a global defence production hub.

Defence Manufacturing Ecosystem in India

- Production: Domestic defence production has grown from ₹46,425 crore in 2014 to a record approx. ₹1.51 lakh crore in FY2025.

- Defence Public Sector Undertakings (DPSUs) continued to anchor production, contributing about 77% of the output.

- Exports: India's defence exports have increased from ₹686 crore in 2013–14 to ₹23,622 crore in 2024–25.

- Role of Private Sector: In 2024-25, defence exports reached ₹15,233 crore from the private sector and ₹8,389 crore from DPSUs.

- Export Destinations: India now exports defence equipment to over 100 countries, with the USA, France, and Armenia emerging as the top buyers in 2023-24.

- Major Export Items: These include bulletproof jackets, patrol boats, Chetak helicopters, Dornier (Do-228) aircraft, Radars and even advanced systems like torpedoes.

- Startups: Funding for India's military-tech start-ups has risen 61 times from Rs. 27 crore in 2016 to Rs. 1,653 crore in 2025, with total investments reaching Rs. 5,248 crore.

Government Initiatives for Defence Manufacturing

- Defence Industrial Corridors (DICs): Two dedicated DICs have been established in Uttar Pradesh and Tamil Nadu.

- Spread across 11 nodes in both states, these hubs are providing the infrastructure and incentives needed to turn India into a defence manufacturing powerhouse.

- Positive Indigenisation Lists: The government has issued Positive Indigenisation Lists that limit imports and encourage local manufacturing.

- Key indigenised technologies include artillery guns, assault rifles, corvettes, sonar systems, transport aircraft, Light Combat Helicopters (LCHs), radars, wheeled armoured platforms, rockets, bombs, armoured command post vehicles, and armoured dozers.

- Innovations for Defence Excellence (iDEX): Launched in April 2018, iDEX has fostered a vibrant ecosystem for innovation and technology development in the defence and aerospace sectors.

- By engaging MSMEs, startups, individual innovators, R&D institutes, and academia, iDEX has provided grants of up to ₹1.5 crore to support the development of cutting-edge technologies.

- Liberalized FDI Policy: Allows up to 74% FDI under the automatic route and beyond 74% (up to 100%) through the Government route.

- Since April 2000, the total FDI in defence industries stands at Rs 5,516.16 crore.

- Defence Testing Infrastructure Scheme (DTIS): It aims to boost indigenisation by providing financial assistance for setting up eight Greenfield testing and certification facilities in the aerospace and defence sector.

- Technology Development Fund (TDF): Established to promote self-reliance in Defence Technology as a part of the 'Make in India' initiative.

- DefExpo: It was conceptualised in 1998 and has evolved as a flagship platform for showcasing India's defence industrial capabilities and promoting defence exports.

Challenges to Atmanirbharata in Defence Manufacturing

- Limited Fiscal Space: Fiscal constraints, competing developmental priorities and the structural burden of revenue expenditure continue to limit the pace at which indigenization can proceed.

- Out of the total allocation made to the Ministry of Defence, only 27.95% of the Defence Budget allocation is for capital expenditure.

- Lack of Technological Innovation: While Indian defence planners have begun to prioritise cyber, electronic warfare, space and unmanned technologies, budgetary allocations for these domains remain modest compared to investments in conventional platforms.

- Import Dependence: India continues to depend on foreign suppliers for critical technologies and high-end platforms such as aero engines, propulsion modules, advanced materials, sensors etc.

- Fragmentation of Defence Innovation Landscape: Although India has created multiple DRDO–academia–industry collaboration frameworks, defence R&D remains fragmented in practice, with cooperation often project-specific rather than system-wide.

- Unlike in Western countries, where most R&D occurs in the private sector, in India, it is dominated by the government and public-sector entities.

- Lack of Input Enablers: Advanced defence production requires reliable capital investments, precision machining and tooling, testing facilities, materials laboratories and secure digital networks.

- Insufficient Skilling: While India produces a large number of engineering and science graduates each year, persistent concerns remain regarding their employability.

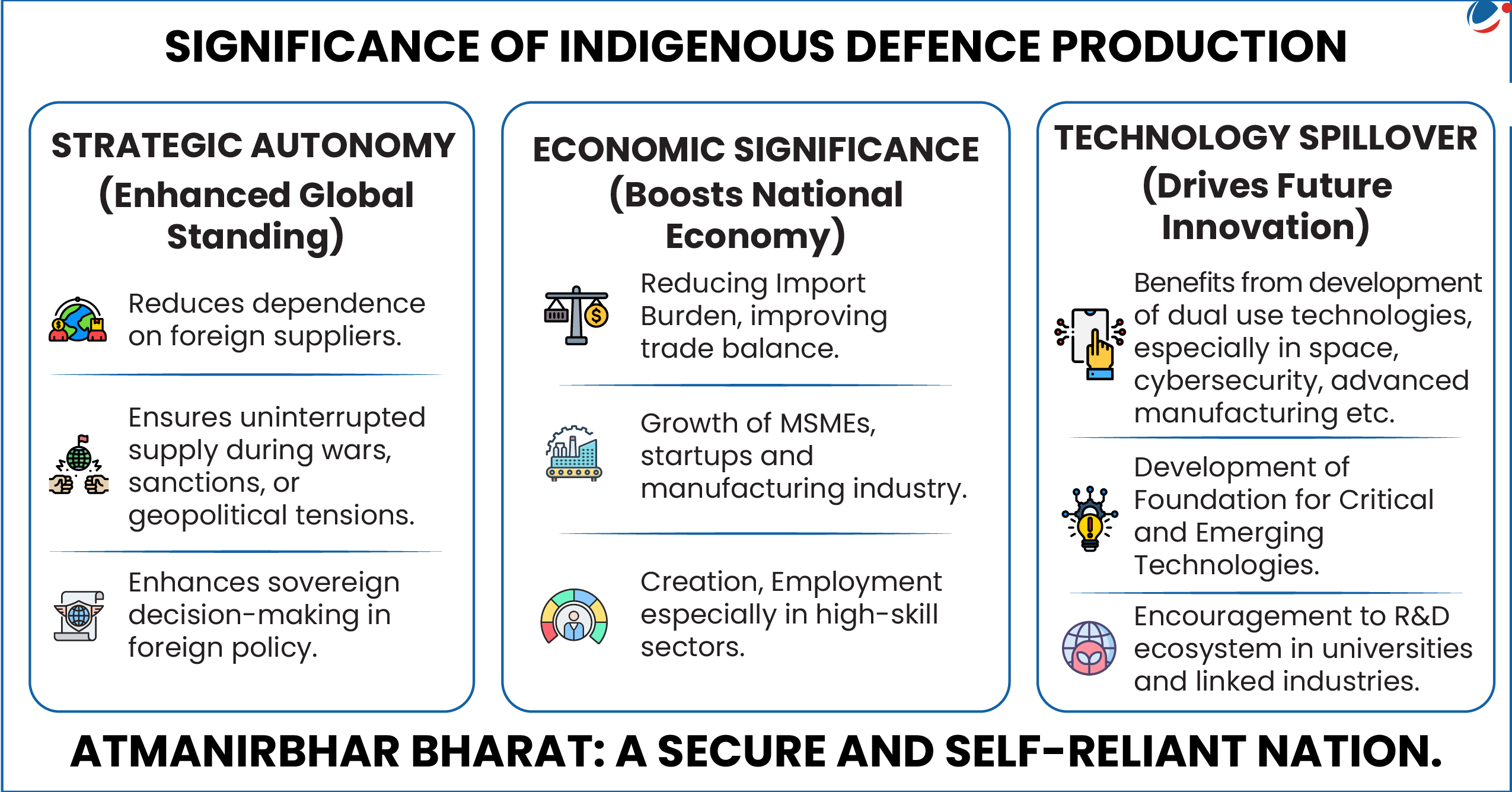

Conclusion

Atmanirbharta in Defence has expanded production numbers, diversified the supplier base, and altered the political discourse and public awareness around defence production. By deepening public–private synergy, prioritising critical technologies and positioning exports as a strategic instrument of diplomacy, India can transition from being a major arms importer to a trusted global defence manufacturing hub. In doing so, defence indigenisation will not only enhance national security but also become a catalyst for industrial modernisation, strategic autonomy and long-term economic resilience.