Why in the News?

Recently, the Supreme Court in a judgement highlighted anomalies in the SARAFESI Act, 2002 and SARFAESI Rules 2002.

Key Observation of Supreme Court

- SC highlighted a contradiction between Section 13(8) of the SARFAESI Act, 2002 and Rules 8 & 9 of the SARFAESI Rules, 2002.

- Contradiction:

- Section 13(8) (post-2016 amendment): Borrower loses their statutory right to pay back the debt in full and recover the secured asset, once the auction notice is published.

- Rules 8 & 9: Indicate borrowers still have a window to redeem even after publication, up until the auction date.

- Court's Interpretation:

- "Publication of notice" under Section 13(8) must be read in line with the procedural steps under the Rules.

- Borrower's right to redeem extinguish only after proper publication (newspaper, personal service, email, etc.) of auction notice.

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002

- Objectives:

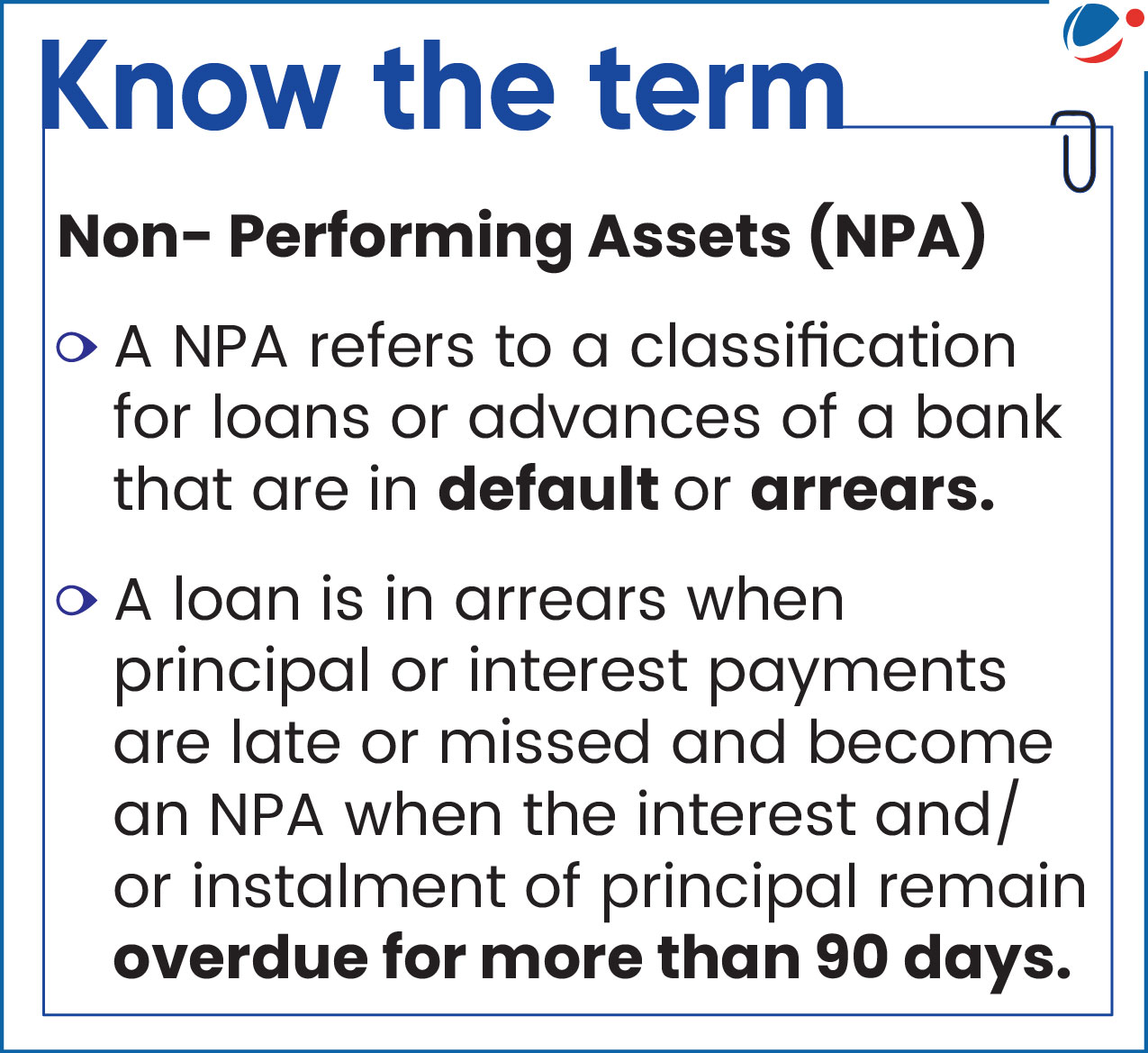

- Recovering the financial institutions' and banks' non-performing assets (NPAs) in a timely and effective manner.

- Cooperative Banks are also covered under it.

- Allows financial organisations and banks to sell residential and commercial assets at auction if a borrower defaults on his or her debt.

- Recovering the financial institutions' and banks' non-performing assets (NPAs) in a timely and effective manner.

Key Features of the Act

- NPA Classification and Notices: Loans are classified as NPAs per RBI guidelines, with a mandatory 60-day demand notice to borrowers before action to recover the asset.

- Key Methods of Recovery:

- Securitisation: Involves transactions where risk of recovery in stressed assets is distributed, among investors, by repackaging such assets into tradable securities with different risk profiles.

- Asset reconstruction: Act provides for the creation of the Asset Reconstruction Companies (ARCs), registered and regulated by RBI.

- ARC is a financial institution that buys the Non-Performing Assets (NPAs) or bad assets from banks and financial institutions so that the latter can clean up their balance sheets.

- Court-Free Enforcement: Secured creditors like banks and financial institutions, can take possession and sell assets except for agricultural land under Section 13 without judicial approval.

- Central Database: Established Central Registry for registration of transaction of securitisation and reconstruction of financial assets.

- Borrower Rights: Borrowers can approach the Debt Recovery Tribunal (DRT) to rectify their grievances against the creditor or authorised officer.

- DRT are established under the Recovery of Debts and Bankruptcy Act, 1993.

- Working:

- After the declaration of the account or asset as NPA, banks or financial institutions direct defaulting borrowers to discharge their liabilities within a 60 days period.

- When failed to comply with the notice, then the bank or financial institution takes action.

Key Issues/challenges associated with the SARFAESI Act

- Exclusion of Certain Borrowers: The Act is not applicable on loans under ₹1 lakh and in cases where 80% of the loan has already been repaid.

- Procedural and judicial delays: Borrowers often approach Debt Recovery Tribunals (DRTs) to seek a stay on possession proceedings.

- Complexities in Asset Recovery: Lenders face challenges in identifying and liquidating collateral, e.g. transfer of assets to third parties.

- Sub-optimal performance of the ARCs: Banks and FIs could recover only about 14.29% of the amount owed by borrowers in stressed assets sold to ARCs from FY04 to FY13.

- Socio-Economic Impact: Forced asset dispossessions can lead to loss of livelihoods, increased indebtedness, and social instability, highlighting the need for a balanced recovery framework.

- Other: Infringement of Borrowers' Rights (Misusing of powers by creditors), disputes in valuation of the assets, exclusion of unsecured creditors etc.

Other initiatives for Securitisation and Reconstruction of Financial Assets/Resolving NPAs

|

Way Forward

- Harmonise Law and Rules: SC has urged the Ministry of Finance to make necessary changes to resolve anomaly issues.

- Harmonization with IBC: The SARFAESI Act should be harmonized with the IBC to ensure a cohesive and comprehensive framework for the resolution of stressed assets.

- Technological Integration: Leverage AI and data analytics for asset valuation and monitoring.

- Specialized Debt Recovery Tribunals (DRTs): With enhanced operational capacities to expedite the resolution of disputes.

- International Best Practices: E.g. United Kingdom's Insolvency Act incorporates debtor protection measures alongside creditor rights, ensuring that recovery does not disproportionately harm individuals/small businesses.

Conclusion

The Supreme Court's ruling clarifies redemption rights and reinforces purchaser protections under SARFAESI, but inconsistencies between the Act and its Rules continue to create uncertainty. Streamlining these provisions, strengthening institutional mechanisms like DRTs and ARCs, etc. is essential to ensure quicker resolution of NPAs.