International Monetary Fund (IMF) slightly upgraded India’s GDP growth forecast for FY27 to 6.5% in its latest WEO Report.

- Global growth is projected to slow to 3.1% in 2026 and 3.2% in 2027.

- Also India slipped out of world's top five economies in nominal GDP terms to be 6th largest economy preceded by USA, China, Germany, Japan, and UK.

About WEO

- It presents analyses and projections of the world economy in the near and medium term.

- Published twice a year with updates in between.

- Other Reports by IMF: Global Financial Stability Report, Fiscal Monitor.

Food and Agriculture Organization (FAO) Food Price Index rose to 128.5 points in March 2026, driven by higher energy costs amid Middle East tensions.

FAO Food Price Index

- A measure published by the Food and Agriculture Organisation (FAO) tracking monthly changes in international prices of a basket of food commodities.

- Base year: 2014–16.

- Composition: Includes five major commodity groups—cereals, vegetable oils, dairy, meat and sugar.

KABIL secures environmental clearance for deep exploration of five lithium blocks in Argentina.

- Lithium is a soft, silvery-white alkali metal and has the lowest density of all metals.

- Argentina, Bolivia and Chile (Lithium Triangle) hold more than 75 percent of the world’s lithium supply.

About KABIL

- Overview: Established in 2019 as a Joint Venture Company of the National Aluminium Company Ltd. (NALCO), Hindustan Copper Ltd. (HCL) and Mineral Exploration and Consultancy Ltd.

- Operates under the aegis of Ministry of Mines.

- Objective: It identifies, acquire, develop, process and make commercial use of strategic minerals including Lithium in overseas locations for supply in India.

The Mines Ministry instituted ₹5,000 crore incentive scheme incorporated under the Scheme for Special Assistance to States for Capital Investment (SASCI) for FY 2026-27.

- Incentive scheme aims to facilitate and expedite mine operationalization, increase mineral production, enhance revenue collection by States, and improve overall governance of the mining sector.

- Scheme incentive to states and UTs under three reform areas – Implementation of mining reforms, Mine operationalization, and State Mining Readiness Index (SMRI) based reforms.

About SASCI

- Type: Central Sector.

- Ministry: Ministry of Finance.

- Aim: Financial assistance provided to the State Governments in the form of a 50-year interest free loan for capital expenditure.

Article Sources

1 sourceUnion Minister of Communications released revised guidelines for the Technology Development and Investment Promotion (TDIP) Scheme for 2026-31.

- Revised guidelines expanded the scope of the scheme to include startups, MSMEs, academia, research institutions, telecom service providers.

About TDIP Scheme

- Objective: designed as a comprehensive support framework to enable Indian telecom entities to actively contribute to promote innovation, and enhance India’s competitiveness in next-generation telecommunications technologies, including 5G Advanced and 6G.

- Implementation Agency: Telecommunications Standards Development Society, India (TSDSI), Telecom Centres of Excellence, India (TCoE) and Telecommunications Consultants India Limited (TCIL).

Article Sources

1 sourceGovernment expanded coverage of RELIEF Scheme amid West Asia crisis.

About RELIEF Scheme

- It is a time-bound intervention under the Export Promotion Mission (EPM).

- Objective: Help Indian exporters deal with high freight costs, rising insurance premiums and war related export risks.

- Nodal and Implementing Agency: ECGC Ltd. (Formerly Export Credit Guarantee Corporation of India Ltd.), wholly owned by Government of India (Ministry of Commerce & Industry).

- Key Features

- MSME-Focused Assistance: Ensuring reimbursement support for High logistics costs and surcharges.

- Export Cycle Coverage: For End-to-end support for shipment planning, Insurance etc.

Article Sources

1 sourceGovernment notifies extension of RoSCTL Scheme up to 30th September 2026.

About the scheme

- Launched: In 2019 by the Ministry of Textiles.

- Aim: to zero-rate textile exports by rebating all embedded State and Central taxes and levies, not covered under any other scheme.

- Mechanism: Rebates are issued as Duty Credit Scrips which can be sold or used to pay custom duty.

- Benefits: Flexibility, enhanced export competitiveness, cost reduction etc.

Article Sources

1 sourceThe Ministry of Textiles has launched an initiative called ‘Vishwa Sutra – Weaves of India for the World’.

About Vishwa Sutra

- Initiated by the Office of the Development Commissioner (Handlooms) in collaboration with the National Institute of Fashion Technology.

- Aim: To present Indian handlooms in a contemporary global design framework.

Article Sources

1 sourceNational Statistics Office (NSO), Ministry of Statistics and Programme Implementation (MoSPI), launched Annual Survey of Incorporated Services Sector Enterprises (ASISSE).

About ASISSE

- First annual survey covering incorporated service enterprises across all States/UTs (FY 2024-25 reference).

- Coverage: Incorporated service sector enterprises registered under the Companies Act, 1956, or Companies Act, 2013, or Limited Liability Partnership Act, 2008.

- Covers sectors like trade, transport, IT, health, education, hospitality.

- Aim: To build a reliable database for policymaking and economic analysis.

- Uses Goods and Services Tax Network (GSTN) database; ~1.21 lakh enterprises surveyed.

- Complements ASI (Annual Survey of Industries) and ASUSE (Annual Survey of Unincorporated Sector Enterprises) for holistic non-agricultural economy data.

Article Sources

1 sourceIncome Tax Act, 2025 replaces the six-decades-old Income Tax Act, 1961 with objective to enhance predictability, transparency, reduce compliance burden, and offer taxpayers a streamlined and simplified tax filing process.

Key provisions of the Act

- Simpler language and Framework: Act has been condensed from 819 to 536 Sections, and 390 to 190 Forms.

- Provisions of Minimum Alternate Tax (MAT) and Alternate Minimum Tax (AMT) have been separated into two sub-sections.

- MAT bring into the tax net "zero tax companies" which in spite of having earned substantial book profits and having paid handsome dividends, do not pay any tax due to various tax concessions and incentives provided under the Income-tax Law.

- AMT has similar provisions as MAT which is applicable to non-corporate tax payers.

- The provisions of MAT are applicable to a corporate taxpayer only.

- "Tax Year" Concept: The traditionally separate concepts of Financial Year (FY) and Assessment Year (AY) have been merged into a single, unified term: "Tax Year".

- Stability in Core Tax Elements

- Tax rates and regimes for individuals and corporations remain unchanged.

- There are no changes in offences and penalties.

- Most definitions have also been retained.

- Faceless collection of information and assessment of tax cases.

- Undisclosed Income: The definition of undisclosed income for assessing search cases, which previously included money, bullion, jewellery, or other valuable articles, is expanded to include virtual digital assets.

- Virtual Digital Space Access: Income tax authorities are now allowed to gain access to a virtual digital space during search and seizure proceedings.

- A "virtual digital space" is defined broadly to include email servers, social media accounts, online investment and trading accounts, and websites for storing details of asset ownership.

Article Sources

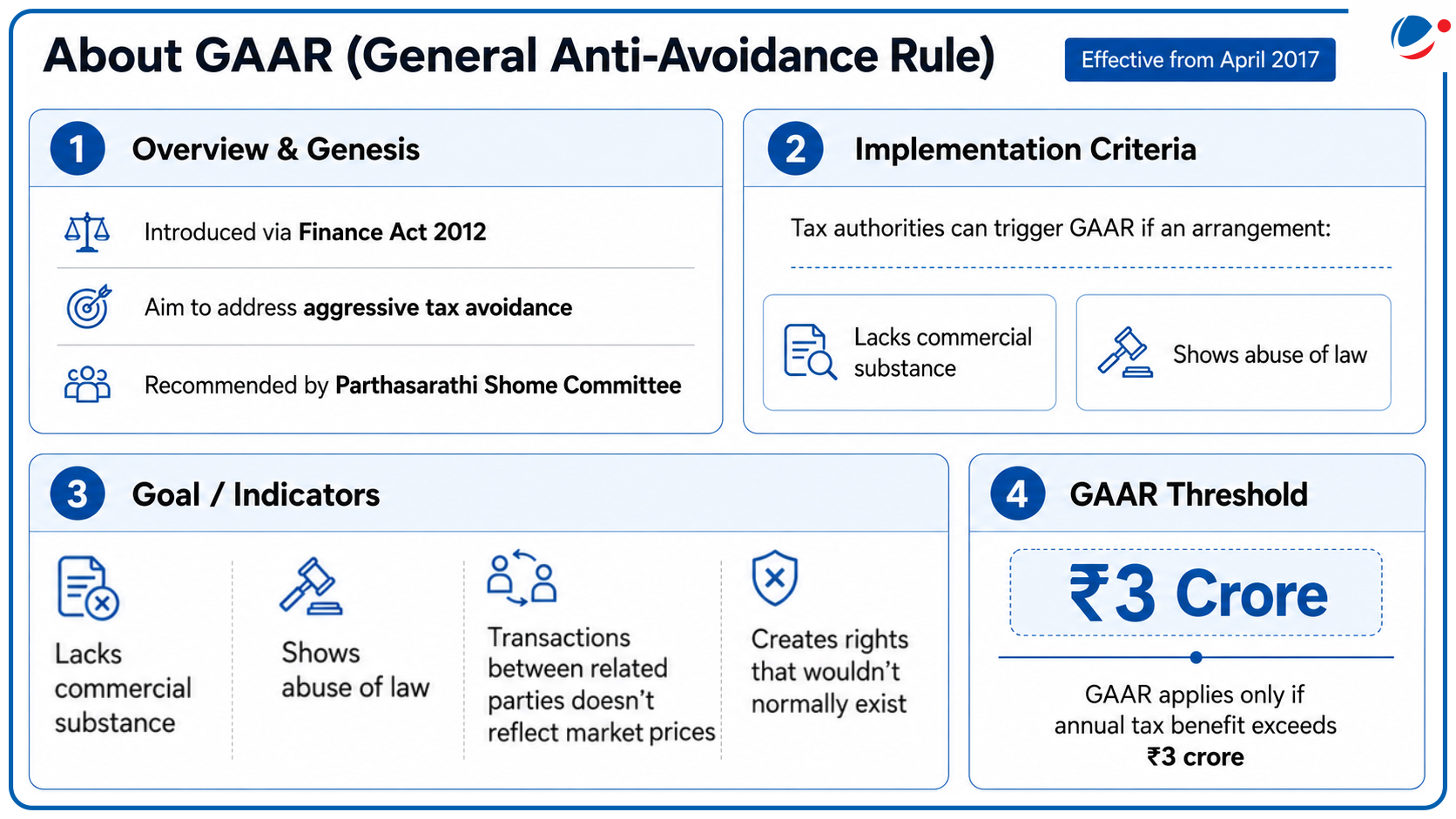

1 sourceIndia amended Income Tax Rules, 2026, under Income Tax Act, 2025, to exclude investments made before 1 April 2017,from GAAR

- This removed ambiguity around grandfathering.

- Grandfathering lets investments made before a specified date enjoy old tax rules despite later changes.

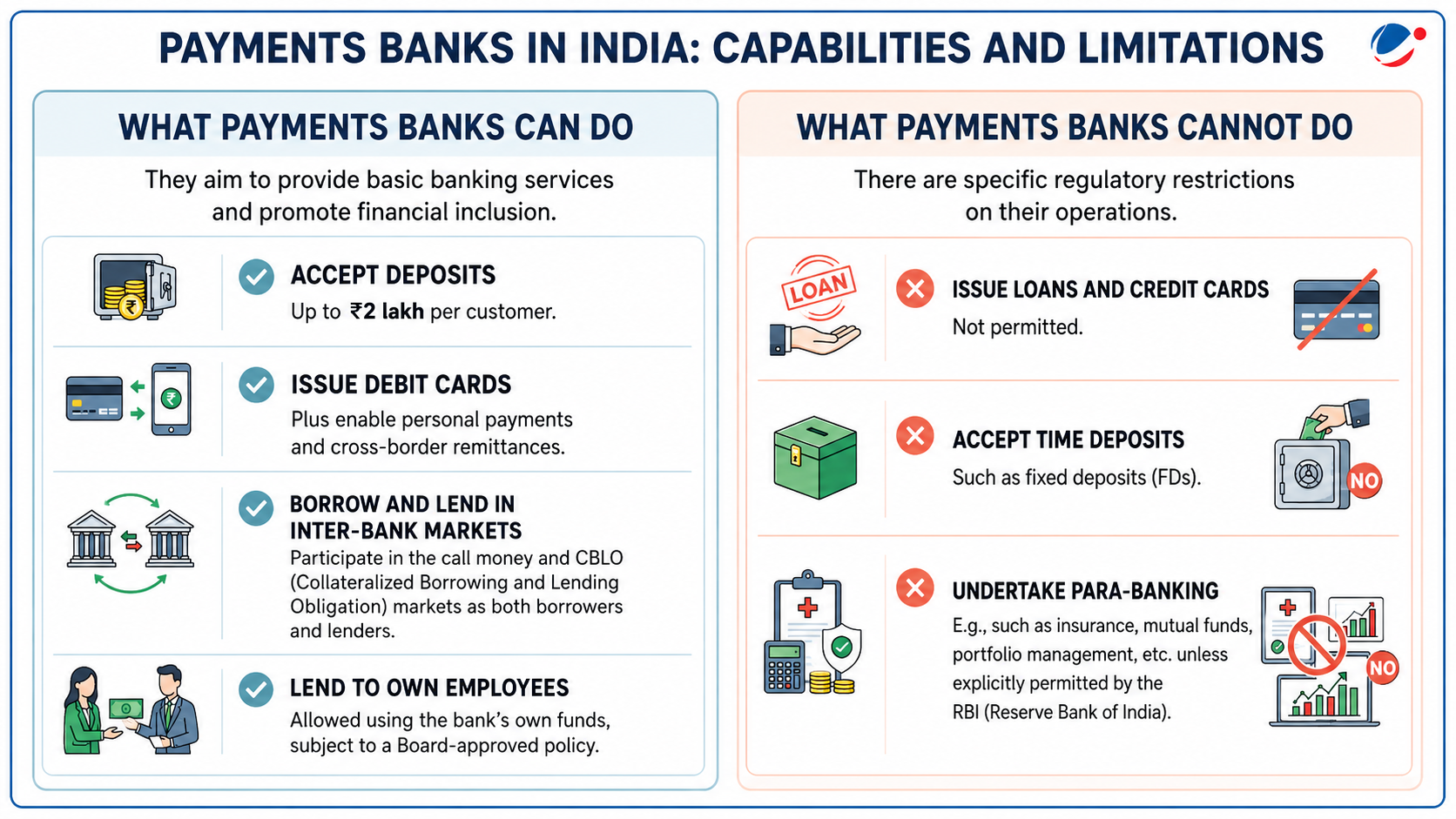

Reserve Bank of India (RBI) canceled Banking Licence of Paytm Payments Bank.

- According to the RBI, Paytm Payments Bank failed to adhere to the Guidelines for Licensing of Payments Banks under the Banking Regulation Act, 1949.

About Payment Banks

- Recommended by the Nachiket Mor Committee in 2014.

- Definition: A Payment Bank is a financial institution set up to operate on a smaller scale with minimal credit risk under Differentiated banking licenses (DBL)

- DBL are specialized licenses designed to serve specific customer segments.

- Other Financial Institution under DBL: Small Finance Banks.

- DBL are specialized licenses designed to serve specific customer segments.

- Objectives: To promote financial inclusion through serving unbanked and underbanked populations (E.g. Migrant workers, low-income households).

- Advantages: Boost digital payments, offer a safe alternative for small transactions, and reduce cash dependency.

- Regulatory Framework:

- Registration: Companies Act, 2013.

- Governance: Banking Regulation Act, 1949; RBI Act, 1934; Foreign Exchange Management Act, 1999; Payment and Settlement Systems Act, 2007.

- Capital Requirement: They must have a minimum paid-up capital of ₹100 crore (promoters’ share to be ≥40% for the first five years).

- 75% funds in SLR securities, 25% with banks.

Article Sources

1 sourceReserve Bank of India (RBI) has directed to bar banks from NDD contracts in rupee.

About NDD

- Derivative contract where two parties agree on future exchange rate for rupee, but settle the difference in cash, usually in US dollars.

- These trades take place offshore, outside the control of RBI.

- They were developed in response to restrictions that constrained access to onshore markets and are widely used by foreign investors, hedge funds and global banks who cannot freely access the Indian rupee market.

Recently, a private bank took action against individuals for alleged involvement in mis-selling of Additional Tier-1

(AT-1) bonds.

About AT-1 Bonds

- Type of debt instrument issued by banks to strengthen their capital base.

- Key Features:

- Perpetual: Unlike regular bonds (government, corporate, etc) with a fixed maturity date, AT-1 bonds have no maturity date.

- Convertible to Equity: In a financial distress situation.

- High Risk, High Reward: Due to their risk profile, they offer higher interest rates than traditional bonds.

- Issued by: Banks at the direction of the RBI.

RBI has introduced a cap on banks’ NOP in Indian rupee, limiting it to $100 million at the end of each business day.

- This is far lower than earlier limit of 25% of bank’s total capital.

About NOP

- It represents the difference between a bank’s foreign currency assets and liabilities.

- It reflects the extent of a bank’s exposure to currency fluctuations and a higher NOP indicates a larger exposure on the currency.

The Reserve Bank of India notified limits for investment in debt and sale of Credit Default Swaps by Foreign Portfolio Investors (FPIs) for FY 2026-27.

- The limits for FPI investment in Government Securities (G-Secs), State Government Securities (SGSs) and corporate bonds remain unchanged.

About Credit Default Swaps

- Definition: It is a financial derivative instrument that allows an investor to swap or offset their credit risk with that of another investor.

- Working Mechanism: It works like an insurance on bonds, where the buyer pays regular premiums and the seller pays if a default or restructuring occurs.

- Uses: Used for hedging, speculation, and arbitrage, credit risk management.

- Risks: Counterparty risk, complexity.

Article Sources

1 sourceIRDAI (Insurance Regulatory and Development Authority of India) has introduced Ind AS (Indian Accounting Standards) based Financial Reporting Framework for the Insurance Sector.

- It aims to align the Indian insurance sector with globally accepted standards.

- It applies to all categories including life, general, standalone health insurers, and reinsurers.

About Ind AS Framework

- Overview: They are a set of financial reporting standards implemented in India to harmonize local accounting practices with the International Financial Reporting Standards (IFRS).

- Primary Goal: To enhance the global accessibility, transparency, and reliability of financial statements produced by Indian companies.

- Implemented by: Ministry of Corporate Affairs (MCA).

The US announced a 100% ad valorem duty on the import of patented pharmaceuticals and associated ingredients.

- This will not include generic drugs “at this time,” having a limited impact on India.

- The US is India’s largest market for pharmaceutical exports, accounting for an almost 40% share.

About Ad Valorem Duty

- An ad valorem tariff is a customs duty calculated as a percentage of the total value of imported goods.

- Unlike fixed-fee tariffs, which are based on weight or quantity, these tariffs fluctuate depending on the declared value of the product.

- These tariffs are widely used to regulate trade, protect domestic industries, and generate government revenue.

FoF2.0 builds upon FoF for Startups (FFS 1.0) launched in 2016 under Startup India Action Plan enabling access to venture capital for startups across stages and sectors.

- Venture Capital (VC) is an early-stage equity funding that comes with active guidance for startups with high growth expectations.

Key Highlights of the Scheme

- Total corpus: ₹10,000 crore

- Ministry: Ministry of Commerce and Industry.

- Eligibility: Alternative Investment Funds (AIFs) spread across 16th and 17th Finance Commission cycles.

- AIF refers to privately pooled investment vehicle which collects funds from sophisticated investors (Indian/foreign) for investing as per defined investment policy.

- Structure: Scheme will contribute to corpus of SEBI-registeredAIFs for investing in equity and equity-linked instruments of ‘startups’.

- Selection process for AIFs: Involves screening by Venture Capital Investment Committee (VCIC) comprising of veterans from startup ecosystem.

- Monitoring and Governance: ‘Empowered Committee (EC)’ chaired by Secretary, DPIIT (Department for Promotion of Industry and Internal Trade).

- Implementation:Small Industries Development Bank of India (SIDBI) [also the implementing agency of FFS 1.0]

- In addition, another domestic IA(s) will be selected for implementation.

- Segmented approach:

- AIFs supporting deep tech: Startups engaged in developing novel solutions addressing complex problems involving longer R&D cycles, higher costs.

- Smaller AIFs (Micro VCs): Supporting early growth stage startups.

- AIFs supporting tech-driven innovative manufacturing startups: Manufacturing-oriented champion sectors under “Make in India”.

- AIFs supporting sector/stage agnostic startups.

Article Sources

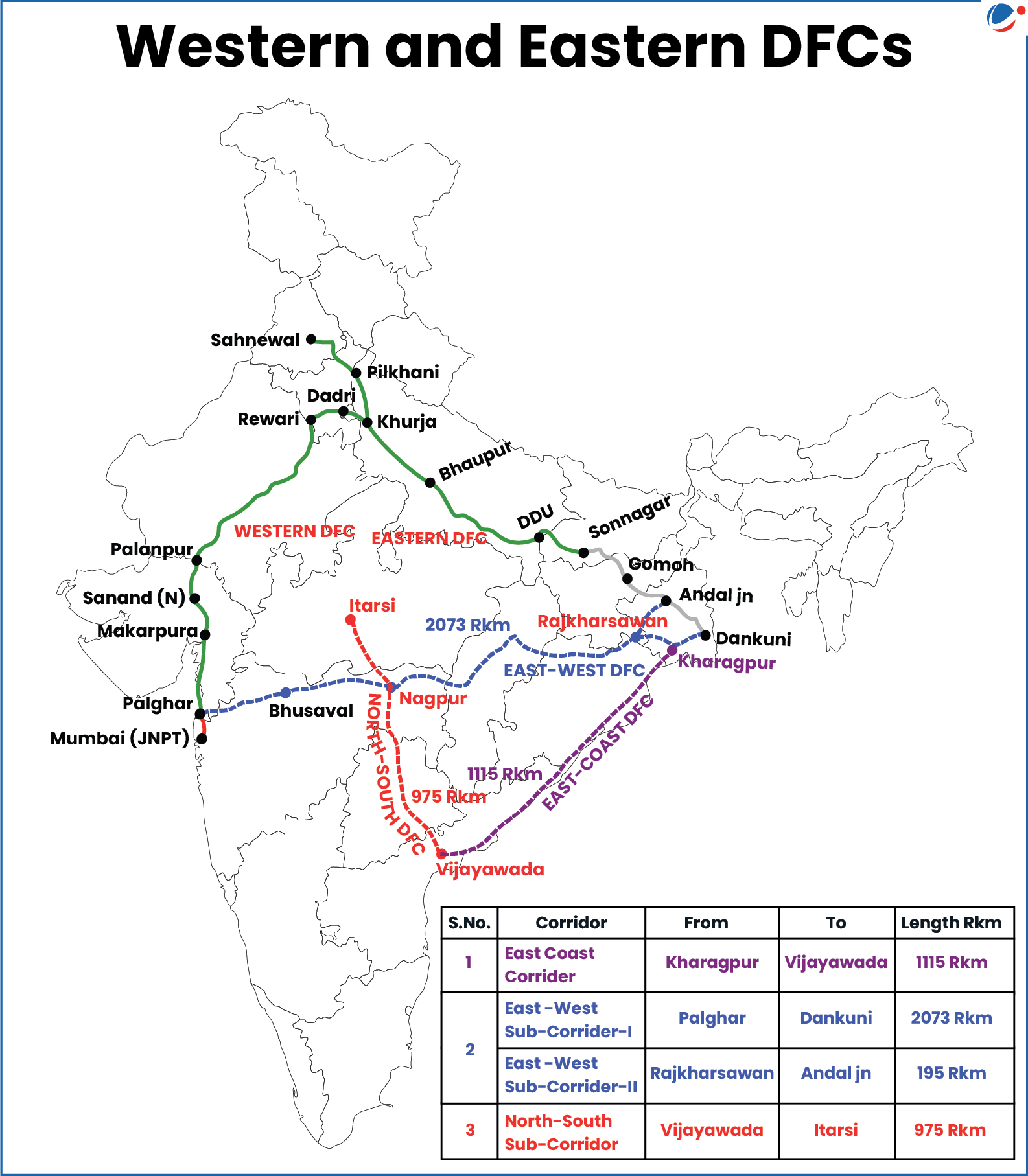

1 sourceWestern DFC is a 1,506-km project stretching from Dadri in Uttar Pradesh to Jawaharlal Nehru Port Terminal (JNPT) in Maharashtra.

About Dedicated Freight Corridor (DFC)

- Genesis: DFC Project was conceived in 2005 and aims at building dedicated freight-only railway lines.

- Two DFCs: Eastern DFC (EDFC) and Western DFC (WDFC) were approved in 2008.

- EDFC runs from Ludhiana (Punjab) to Sonnagar (Bihar) with a length of 1337 Km.

- Along with these two, Ministry of Railways has undertaken work towards Detailed Project Reports (DPR) for three new DFCs (currently under examination):

- EDFC runs from Ludhiana (Punjab) to Sonnagar (Bihar) with a length of 1337 Km.

- East-Coast Corridor: Kharagpur to Vijayawada.

- East-West corridor:

- Palghar-Bhusawal-Nagpur-Kharagpur-Dankuni.

- Rajkharsawan - Kalipahari – Andal.

- North-South Sub-corridor: Vijayawada-Nagpur–Itarsi.

- DFCCIL: Established in 2006, Dedicated Freight Corridor Corporation of India (DFCCIL) is a Special Purpose Vehicle set under administrative control of Ministry of Railways.

- It undertakes planning & development, mobilization of financial resources and construction, maintenance and operation of DFCs.

Importance of DFCs

- Ease Congestion: Mixed passenger and freight traffic limits operational flexibility.

- Enhanced Train Speed and Freight Productivity: Designed to handle high-capacity freight trains traveling at speeds of up to 100 km/h.

- Reduce Logistics Cost: Congestion, delays, and uncertain transit times increases costs for industries.

- Cleaner & Safer Transport: Entire DFC network is fully electrified and hence shifting freight movement from road to rail would reduce emissions.

- Alignment with National Infrastructure Goals: DFC is a crucial component of National Rail Plan for creating future-ready rail network by 2030.

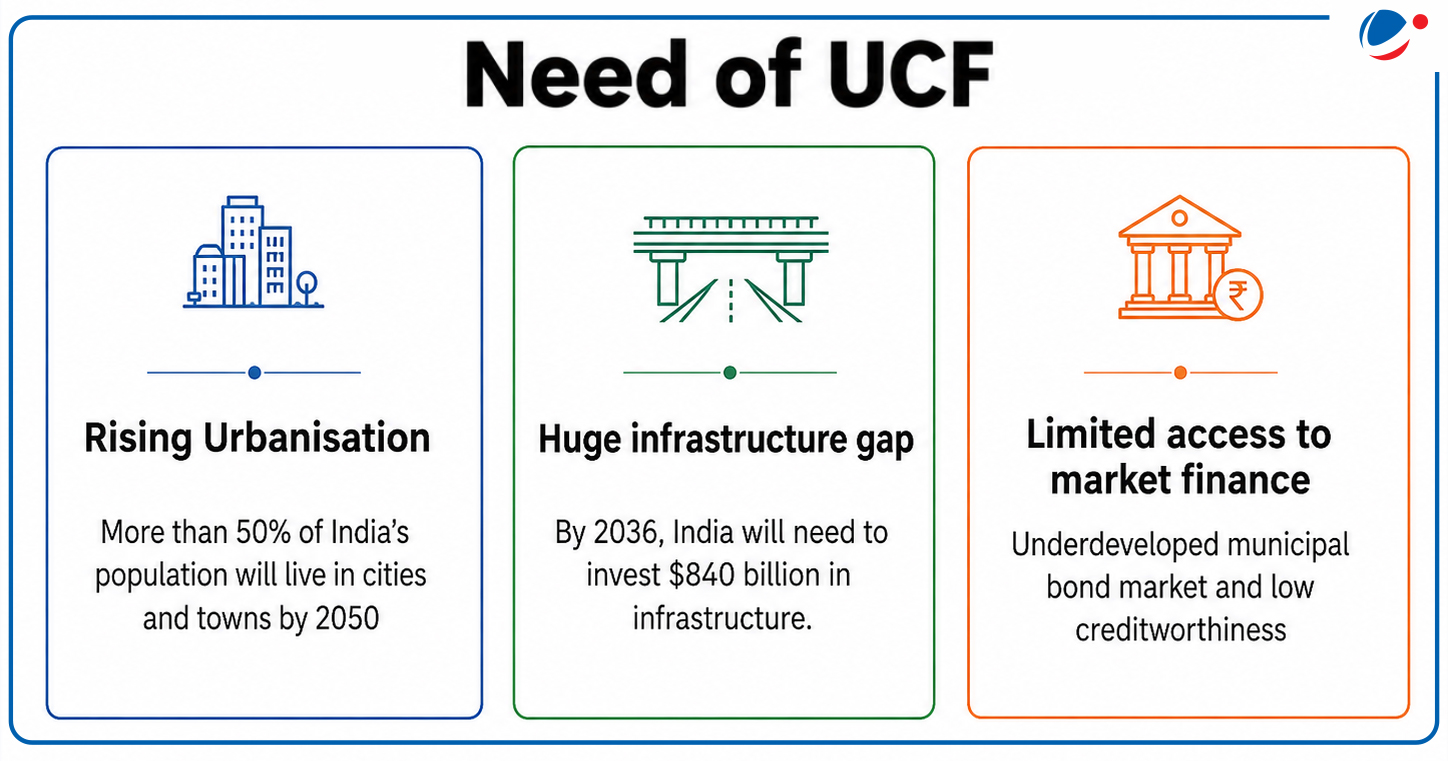

Ministry of Housing and Urban Affairs (MoHUA) launched operational guidelines of Urban Challenge Fund (UCF).

- Along with the guidelines for the UCF, the guidelines for the Credit Repayment Guarantee Sub-Scheme have also been launched.

- UCF will leverage market finance, private participation and citizen- centric reforms for delivery of high-quality urban infrastructure.

About Urban Challenge Fund

- Scheme Type: Centrally Sponsored Scheme

- Fund Allocation: 1 Lakh crore (this will facilitates a total investment of ₹4 lakh crore in next five years)

- Funding pattern:

- 25% of the project cost will be provided through the fund.

- At least 50% must be mobilised from market sources, ensuring private participation.

- The remaining 25% can be contributed by States/UTs/ULBs or raised from the market.

- Focus areas: Creative development of cities’, Cities as growth hubs’, and Water and sanitation’.

- Eligible Cities:

- All cities with a population of 10 lakh or more (2025 estimates);

- All State and Union Territory capitals not covered above; and

- Major industrial cities with a population of 1 lakh or more.

- Implementation period: FY 2025–26 to 2030–31 (with scope for extension)

- Projects already funded under AMRUT 2.0/ SBM 2.0/ other CSS are not eligible under UCF.

Guiding Principles of UCF Implementation

- Market-linked financing: Requires substantial funding from market sources, with limited central support to ensure fiscal discipline.

- Challenge-based selection: Projects chosen through a competitive process focusing on impact and reforms.

- Reform-linked disbursement: Funds released only when governance, financial and planning reforms are undertaken.

- Outcome-based approach: Funding tied to performance, milestones and measurable results.

About Credit Repayment Guarantee Sub-Scheme(CRGSS)

|

Article Sources

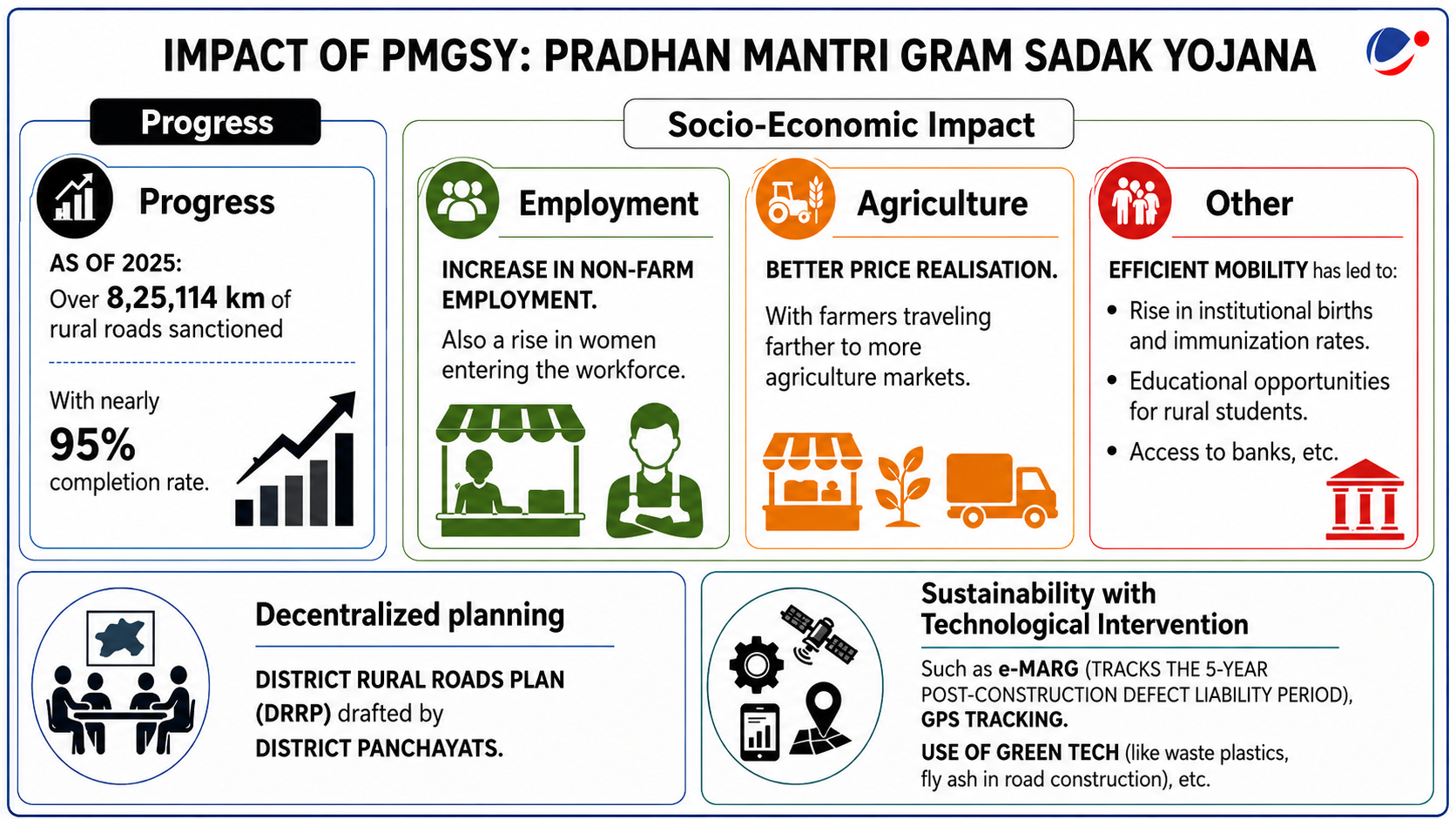

1 sourceUnion Cabinet approved extension of Pradhan Mantri Gram Sadak Yojana-III (PMGSY-III) till March 2028.

Key Features of PMGSY

- Launched: on December 25, 2000, as a flagship centrally sponsored scheme under the Ministry of Rural Development.

- Objective: to alleviate poverty by providing all-weather road connectivity to previously unconnected rural habitations with a population of

- 500 or more in plain areas,

- 250 or more in special category regions, such as the North-Eastern states, Himalayan states, desert areas, and select backward districts.

- Key Phases:

- Phase I (2000): focused on providing initial all-weather connections to eligible unconnected habitations.

- Phase II (2013): Shifted focus to upgrading 50,000 km of the existing rural road network to improve transportation efficiency and support economic hubs.

- For Left Wing Extremism Affected Areas (2016): targeted 44 severely affected districts across nine states to improve both socio-economic development and the mobility of security forces.

- Phase III (2019): Aimed at upgrading 1,25,000 km of Through Routes and Major Rural Links to connect villages directly to Gramin Agricultural Markets, higher secondary schools, and hospitals.

- This phase has now been extended beyond March 2025 up to March 2028.

- Phase IV (2024–25 to 2028–29): Set to construct an additional 62,500 km of roads to connect 25,000 previously unconnected habitations.

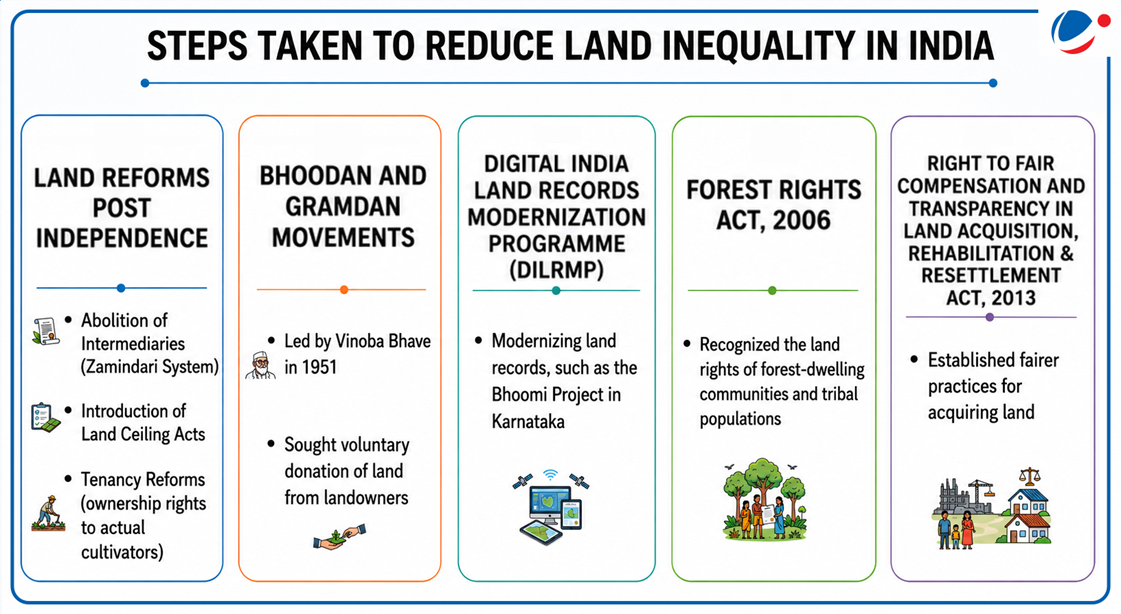

Report titled "Land inequality in India: Nature, history, and markets," encompasses data from ten major Indian states (~ 75% of rural population).

Key Findings of the Report

- Extreme Wealth Concentration: Top 10% of rural households own 44% of the total land area.

- Widespread Landlessness: Nearly 46% of rural Indian households are entirely landless.

- Village-level land Gini Coefficients: extremely high at 71.1.

- Dominant Landlords: In an average village, the single largest landholder controls roughly 12.4% of the land.

- Regional Disparities:

- Highest Inequality: Kerala (Land Gini coefficient at 90).

- Lowest Inequality: Karnataka and Rajasthan (Land Gini coefficients below 65).

- Rates of Landlessness: Punjab highest at 73%.

Key Drivers of Land Inequality in India

- Nature: High productivity facilitates the expansion of large landholdings and drives up landlessness.

- History:

- Colonial Tenure: Regions formerly under the British zamindari (landlord) system exhibit higher inequality, vis-à-vis "princely states".

- Social Stratification: Villages with a higher proportion of Scheduled Caste (SC) populations face higher inequality, due to historical landlessness.

- Markets (Economic Integration): Proximity to economic hubs, such as towns, major highways, railways, banks, and agricultural markets (mandis) is associated with higher land inequality.

- Economic integration alters the profitability of farming relative to non-agricultural activities, incentivizing smallholders to sell their non-viable plots to larger landowners.

Developing nations recently launched the first-ever Borrowers’ Platform at the IMF-World Bank Spring Meetings 2026.

About the Borrowers’ Platform

- Objective: A dedicated forum for peer learning, debt management capacity-building, and strengthening borrower voices in sovereign debt negotiations.

- It is not a debt restructuring forum.

- Members: 30 founding members (including India); Chair-Egypt

- Secretariat: UN Trade and Development (UNCTAD).

- Significance: Provides borrowers who have external debt reaching $11.7 trillion in 2024, a formal coordination mechanism.

- Sovereign debt coordination was long dominated by creditor-led mechanisms like the Paris Club.

WTO Ministerial Conference (MC14) concluded in Yaoundé, Cameroon.

- Ministerial Conference is the highest decision-making body of the WTO, which meets biennially to take decisions on global trade rules.

Key Decisions Adopted at MC14

- Integration of Small Economies: Ministers agreed to improve integration of small economies into the global trading system.

- Strengthening Special & Differential Treatment (S&DT): Enhance implementation of S&DT provisions in the Agreements on Sanitary and Phytosanitary Measures (SPS) and Technical Barriers to Trade (TBT).

- Agreement on SPS lays out the basic rules on food safety and animal and plant health standards.

- Sanitary (human and animal health) and phytosanitary (plant health) measures apply to domestically produced food or local animal and plant diseases, as well as to products coming from other countries.

- TBT Agreement aims to ensure that technical regulations, standards, and conformity assessment procedures are non-discriminatory and do not create unnecessary obstacles to trade.

- Agreement on SPS lays out the basic rules on food safety and animal and plant health standards.

- Fisheries Subsidies Negotiations: Ministers agreed to continue negotiations on fisheries subsidies to develop comprehensive disciplines by the MC15.

Key Outstanding Issues at MC14

|