Why in the News?

The report of the 16th Finance Commission was tabled in the Parliament.

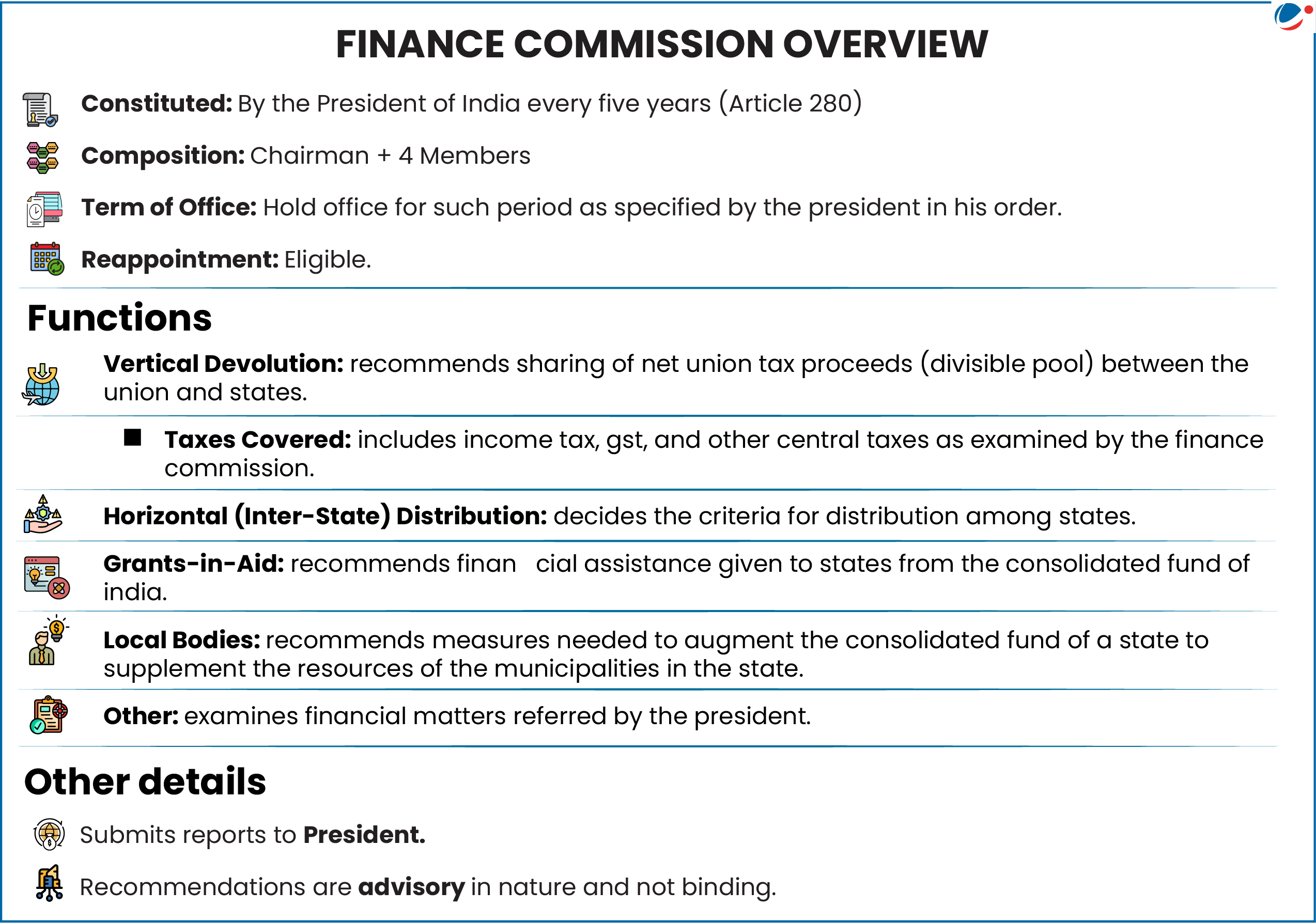

About 16th Finance Commission

- Composition: Dr. Arvind Panagariya (Chairman); T Rabi Sankar, Annie George Mathew, Manoj Panda, and Soumya Kanti Ghosh (Members).

- Award Period: April 1, 2026 – March 31, 2031.

- Terms of Reference:

- Tax Devolution: Distributing net tax proceeds between the Union and States (Vertical) and among the States (Horizontal).

- Grants-in-Aid: Establishing principles for state grants from the Consolidated Fund of India (Article 275).

- Local Body Funding: Augmenting State Consolidated Funds to supplement Panchayat and Municipality resources.

- Disaster Management: Reviewing financing arrangements under the Disaster Management Act, 2005.

Resource Sharing Between Centre and States

- Vertical Devolution: There are three main channels through which resources flow from the Union to the States:

- Divisible Pool: Under Article 270(1), the Union's tax revenues, excluding cesses, surcharges, taxes accruing to the UTs, and the cost of collection, are shared between the Union and the States based on the recommendations of the FC.

- Grants-in-Aid: Under Article 275(1), the FC recommends specific grants to supplement the Consolidated Funds of the States.

- Discretionary Grants: Article 282, the Union provides discretionary grants to States, mainly through the Centrally Sponsored Schemes (CSS).

- Horizontal Devolution: Based on a set of criteria that considers equity (population, area, per capita income, etc.) and efficiency (forest cover, tax effort, fiscal discipline, etc.).

- Each criterion is assigned a weight, which determines the percentage of the States' total share in the divisible pool that will be shared according to that criterion.

Limitations of Finance Commission

- Data Gaps: Relies on official fiscal data that is often incomplete, inconsistent, or outdated.

- Political Pressures: Must balance conflicting stakeholder demands amidst shifting domestic and global landscapes.

- GST Council Overlap: Tax decisions by the GST Council directly alter the revenue pool the FC distributes.

- Centralization vs. Federalism: Grapples with balancing state autonomy against increasing demands for centralized expenditure.

- Limited Local Control: Relies entirely on State Finance Commissions for local government policies, limiting its direct impact on the third tier.

- Advisory Nature: Recommendations are not legally binding, making implementation and oversight difficult.