Why in News?

Unified Payments Interface (UPI) completes 10 Years highlighting its journey from a nascent platform in 2016 to a global digital payments leader in 2026.

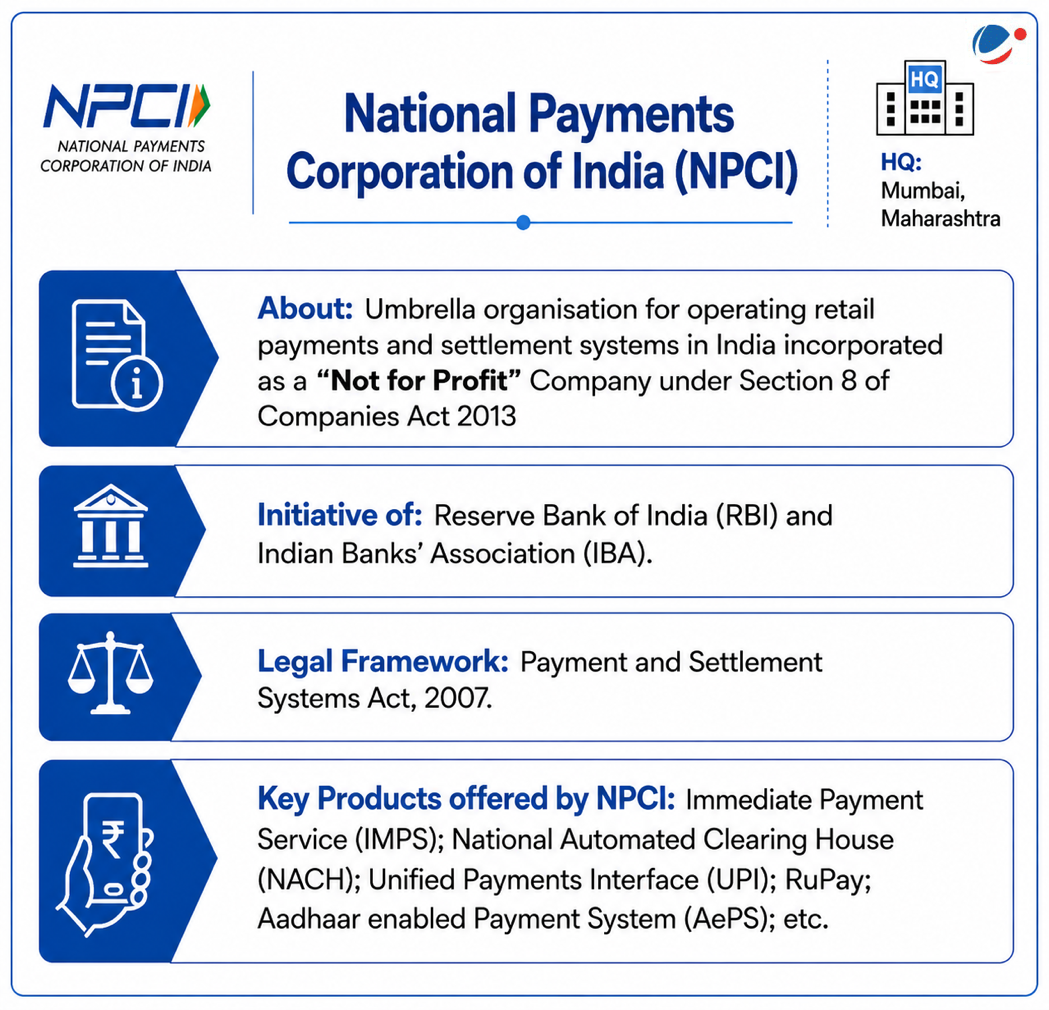

About UPI

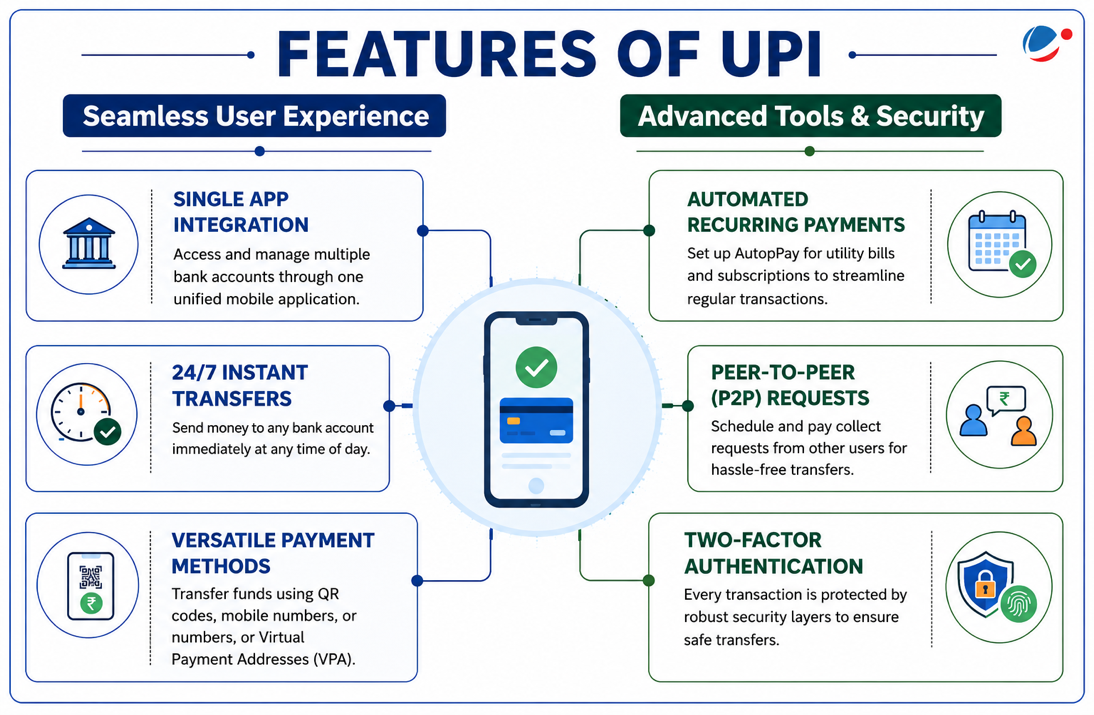

- UPI is a real-time payment system that enables instant, interoperable and secure transactions between individuals and merchants.

- Developed by: National Payments Corporation of India (NPCI)

- It works through institutional participation where each participant bank functions as a Remitter Payment Service Provider (PSP) (processing outgoing transactions) and/or a Beneficiary PSP (receiving funds), with NPCI monitoring performance metrics for all participants.

- Other versions of UPI:

- UPI LITE: On-Device wallet designed to process low value transactions that are below ₹1000 in a faster and pin-less manner.

- UPI LITE X: Allows offline payments without internet connectivity, enhancing the existing UPI LITE functionalities in a much more effective manner.

- UPI Cash Point: Allows withdrawal of cash at local shops and business correspondent outlets using UPI app.

- UPI One World: Prepaid Payment Instrument (PPI) wallet powered by UPI which enables foreign nationals arriving in India and Non-Resident Indians (NRIs) to make UPI-based payments during their stay.

Transformative role of UPI played in India

- Scaling India's Digital Payment system

- Massive transaction Volumes: Transactions grew from 2 crore in FY 2016–17 to 24,162 crore in FY 2025–26, a 12,000‑fold surge in transaction volume.

- Deep penetration of digital payments: In 2025, daily average of about 60 crore UPI transactions were processed.

- Pervasive Network: Connects over 700 banks on a single platform, capturing an 85% share of India's retail digital payments.

- Driving Grassroots Financial Inclusion

- Formalization of economy: Swapped a cash-dependent system for a "one-tap" QR model, integrating small vendors into the formal financial sector.

- Credit for MSMEs: Digital transaction logs help micro-businesses secure formal credit without physical assets.

- Micro-Payments: High-volume, small-value transactions bridge the economic divide between urban hubs and rural zones.

- Person‑to‑person (P2P) transactions shows widespread usage for low-value transfers with 59% transactions below ₹500.

- Catalyzing Financial Innovation & FinTech

- Open Architecture: UPI uses open-API (Application Programming Interface) rails that allow third-party apps like PhonePe and Google Pay to build and innovate rapidly.

- Credit Access: Moves past basic banking by natively supporting instant, pre-approved credit lines linked straight to UPI IDs.

- Projecting Geopolitical Soft Power

- Global recognition: The International Monetary Fund, in its June 2025 report on growing retail digital payments, recognised UPI as the world's largest retail fast payment system by transaction volume.

- Further, as per 2024 ACI Worldwide report titled Prime Time for Real Time, UPI accounts for around 49% of global real time payment transaction volume.

- Global Expansion: UPI is live in over 8 countries, including the UAE, Singapore, Bhutan, Nepal, Sri Lanka, France, Mauritius and Qatar, enabling smooth cross-border retail payments, tourism, and affordable trade remittances.

- DPI Showcase: Serves as a population-scale public good blueprint, offering developing nations a cost-effective alternative to private or state-monopolized networks.

- Global recognition: The International Monetary Fund, in its June 2025 report on growing retail digital payments, recognised UPI as the world's largest retail fast payment system by transaction volume.

Challenges associated with UPI

- Data Security & Cyber Threats: High transaction volumes attract phishing, social engineering, and API vulnerabilities, while compromised biometric data poses unfixable security risks.

- Zero-MDR Sustainability Dilemma: Absence of a Merchant Discount Rate (zero-MDR) on default UPI transactions was critical for grassroots adoption but has created a financial sustainability challenge for banks and third-party application providers (TPAPs).

- Cross-Border Regulatory Hurdles: Expanding internationally requires navigating diverse multi-jurisdictional laws (such as Anti-Money Laundering).

- Market Concentration Risks: The ecosystem is heavily dominated by a few third-party apps (like PhonePe and Google Pay), which can hinder competition.

- Persistent Regional Disparities: Uneven internet penetration and low digital literacy create gaps, leaving rural and underdeveloped populations behind the digital curve.

Conclusion:

The remarkable growth of UPI, both in terms of transaction volumes and geographical reach, highlights its transformative impact on the financial landscape. As UPI continues to expand globally, it is setting new standards for digital payments, empowering citizens, enhancing economic opportunities, and contributing to India's increasing influence in the global financial arena.